Finance Department

The Town Manager and Accounting Staff are responsible for the proper control of finances in the Town; this includes directing or coordinating activities carried on in the areas of accounting, budgeting, treasury and debt administration.

Provides the Town Commission and residents with transparent financial information in a timely and meaningful manner.

Budgeting responsibilities include: development, revision, publication, managing the adoption process, implementation, monitoring the budget throughout the year.

Banking Relations include, but is not necessarily limited to; ensuring transfers are completed, maintaining a professional working relationship with bank officials, bank account reconciliation, interest allocations and the like.

Accounting functions include, but are not necessarily limited to: accounts payable, accounts receivable, pension, compliance with generally accepted accounting principles, compliance with Federal, State, and Town laws and ordinances, cash management, deposits, bank reconciliations, payroll functions and audit process.

FAQs

What is the purpose of the Town Budget?

The budget is an annual financial plan. It specifies the level of municipal services to be provided in the coming year and resources, including personnel positions, capital expenditures and operating expenses needed to provide services.

What is a Fiscal Year?

A fiscal year is a 12 ‐ month operating cycle that comprises a budget and financial reporting period. The Town’s fiscal year begins on October 1 and ends on September 30.

How are Revenues obtained?

From Town levied taxes, state and federal shared revenues and fees for municipal services.

How is Revenue used by the Town?

Revenue is used to pay for salaries, operating supplies, utilities, insurance, and capital purchases.

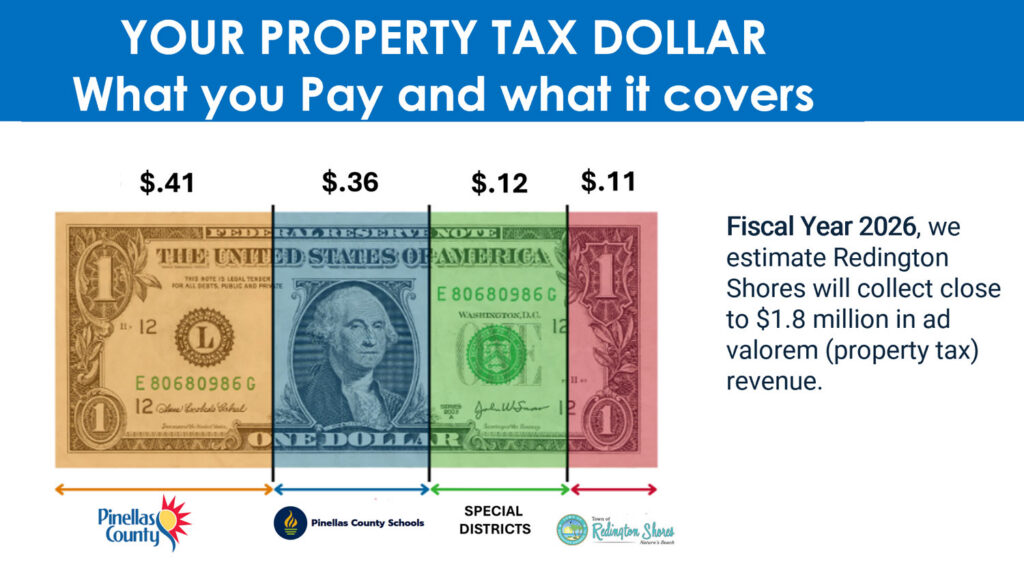

What is Property Rate?

When the Town adopts the annual budget, it determines the tax rate that must be applied on property in order to generate the necessary revenue in addition to all other revenue sources available. The taxable value of all property in the Town is established by the Pinellas County Property Appraiser. The Town has no control over the taxable value of property; it only has control over the Town’s portion of the tax rate that is levied.

What is Homestead Exemption?

Homestead exemption is a constitutional benefit of a $50,000 exemption from the property’s assessed value. It is granted to those applicants with legal or beneficial title in equity to real property as recorded in official records who are bona fide Florida residents living in a dwelling and making it their permanent home on January 1 of the taxable year. The first $25,000 is entirely exempt. The second $25,000 is to be applied to the value between $50,000 and $75,000, and does not include school taxes. For example: If a home’s assessed value is $75,000 or more, the owner would receive the full $50,000 exemption benefit. If the property value is between $50,000 and $75,000, he or she would receive a pro ‐ rated exemption amount. (Example: If the property value is $65,000, the additional exemption would be $15,000, for a total exemption amount of $40,000 (the original $25,000 plus the prorated amount of $15,000.)) The exemption results in approximately a $500 ‐ $800 property tax savings to Florida residents.

What is an Operating Budget?

An operating budget is an annual financial plan for recurring expenditures, such as salaries, utilities and supplies.

What is a Capital Improvement Budget?

A capital improvement budget is both a short and long range plan for the construction of physical assets, such as buildings, streets, sewers, vehicles and other equipment.

For all property tax questions please click here or visit the web site of the Pinellas County Property Appraiser at https://www.pcpao.gov/.

Town of Redington Shores Finances

- Final Budget

FY 2025 – 2026 - Final Budget

FY 2024 – 2025 - Final Budget

FY 2023 – 2024 - Final Budget

FY 2022 – 2023 - Final Budget

FY 2021 – 2022 - Tentative Budget

FY 2021 – 2022 - Final Budget

FY 2020 – 2021 - Tentative Budget

FY 2020 – 2021 - Final Budget

FY 2019 – 2020 - Tentative Budget

FY 2019 – 2020 - Sewer Budget Amendment

FY 2017 – 2018 - Final Budget

FY 2017 – 2018 - Proposed Budget

FY 2017 – 2018 - Final Budget

FY 2016 – 2017 - Final Budget

FY 2015 – 2016 - Final Budget

FY 2014 – 2015 - Final Budget

2013 – 2014 - Final Budget

October 1, 2012 – 2013 - Final Budget

Sep 22, 2011 – 2012 - Final Budget

Oct 1, 2010 – Sept 30, 2011 - Final Budget

Oct 1, 2009 – Sept 30, 2010 - Final Budget

Oct 1, 2008 – Sept 30, 2009 - Final Budget

Oct 1, 2007 – Sept 30, 2008

- Five Year Capital Improvement Plan

FY 2024 – 2028 - Five Year Capital Improvement Plan

FY 2021 – 2025